Italy: Stagflation + Sovereign Stress to 2040

The core macro question: if ECB rates stay elevated while Italian inflation remains sticky and debt keeps climbing, what's the structural trajectory? We ran this exact scenario.

Scenario Configuration

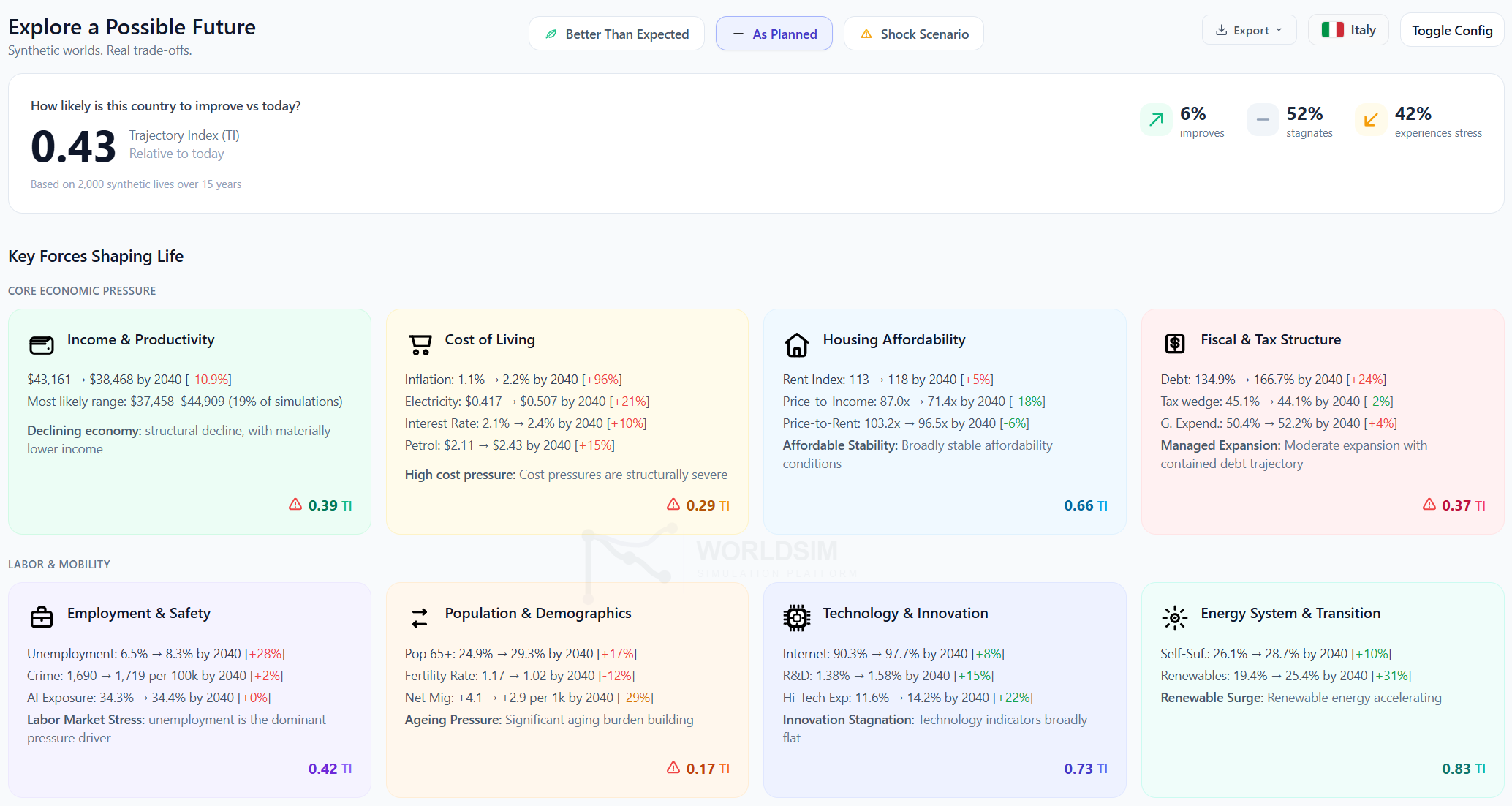

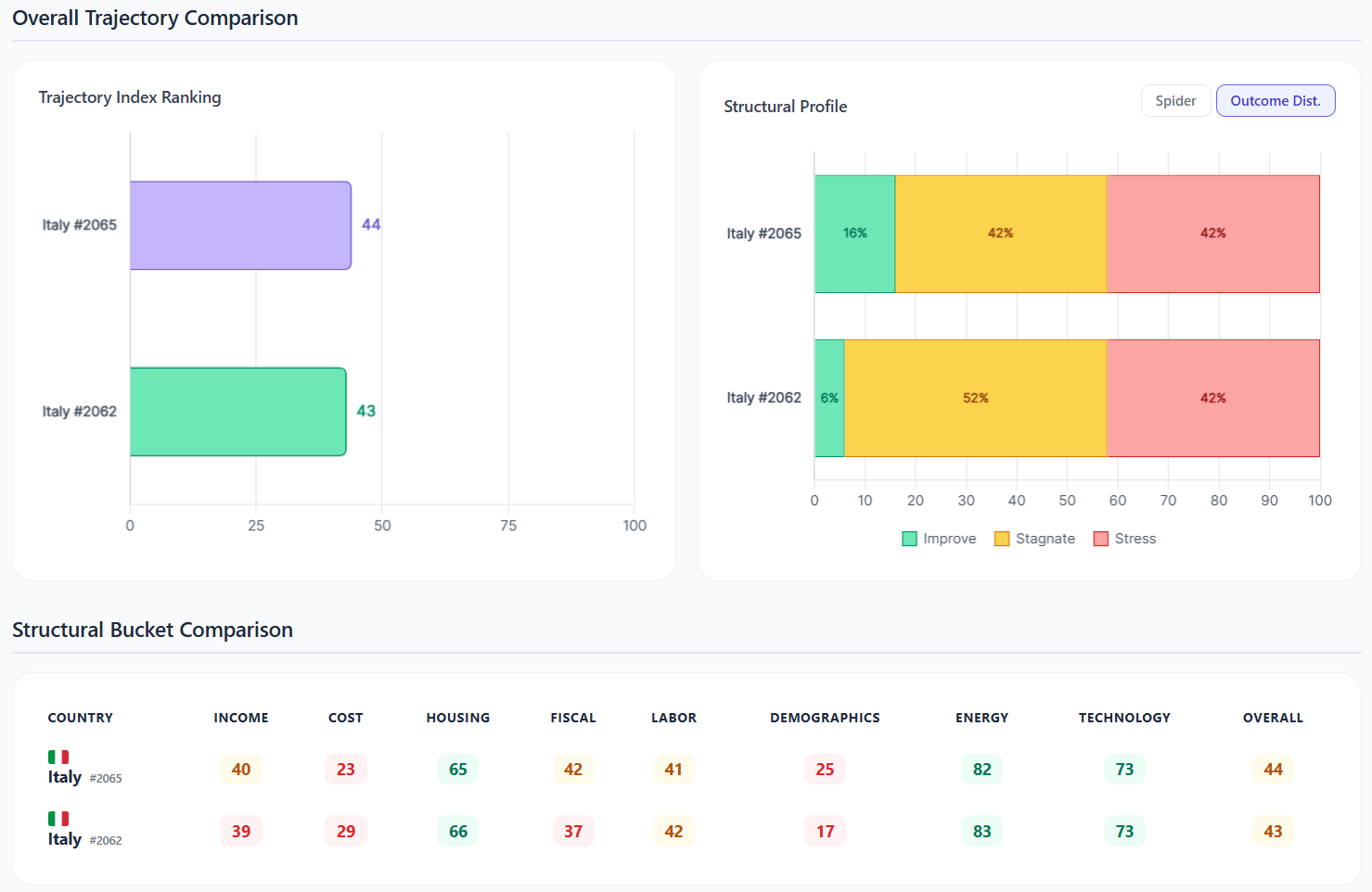

Structural Overview: TI 0.43, 42% of Paths Hit Structural Stress

Italy's Trajectory Index drops to 0.43 under this scenario. Only 6% of simulated paths show improvement. The domain scores tell the story: Income falls to 0.39 (GDP per capita declines 10.9% from $43,161 to $38,468), Fiscal to 0.37 (debt reaches 166.7% of GDP), Cost of Living to 0.29 (inflation nearly doubles), and Demographics to 0.17 (ageing accelerates, fertility drops to 1.02, net migration falls 29%). Housing (0.66), Technology (0.73), and Energy (0.83) remain resilient; this is a fiscal-demographic crisis, not a broad collapse.

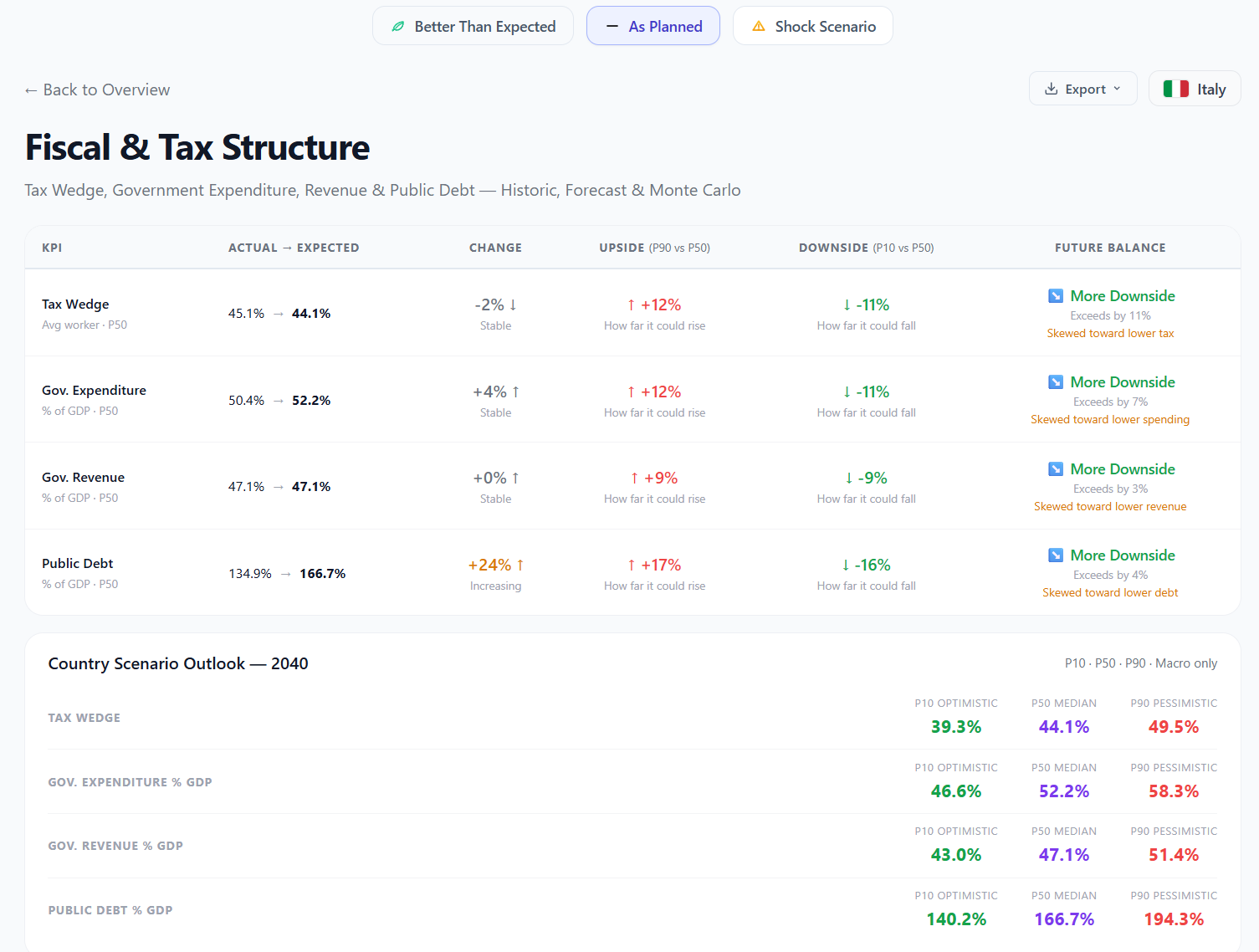

The Sovereign Debt Trajectory: 134% → 167% GDP, P90 Hits 194%

This is the number macro funds care about most. Italian public debt rises from 134% to 166.7% of GDP at the P50 median. But the tail tells the real story: the P90 pessimistic scenario shows debt reaching 194.3% of GDP, the level that triggers restructuring conversations. Government expenditure rises to 52.2% of GDP (P90: 58.3%) while revenue barely keeps pace at 47.1%. The fiscal squeeze is structural, not cyclical.

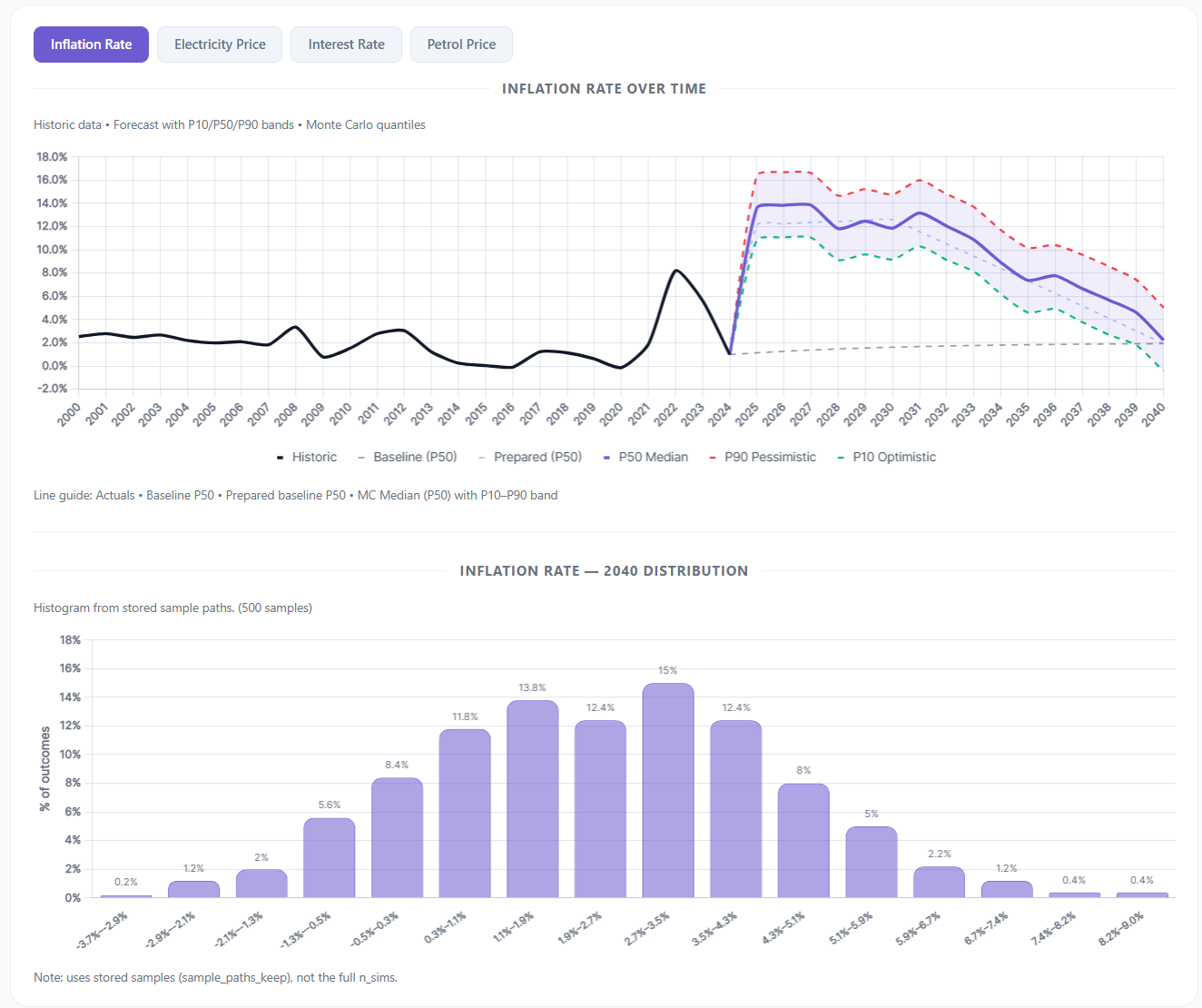

The Inflation Story: P90 Spikes to ~15% Before Reverting

The inflation fan chart shows the acute phase: the P90 pessimistic path spikes toward 15% around 2027 before the coupling rules pull it back. The P50 median settles around 8-10% during the stress period, eventually reverting to ~2-3% by 2040. The 2040 distribution histogram shows the fat tail clearly: most outcomes cluster around 3-4%, but a meaningful fraction remains above 5%. This is the inflation regime risk that drives the rate path trade.

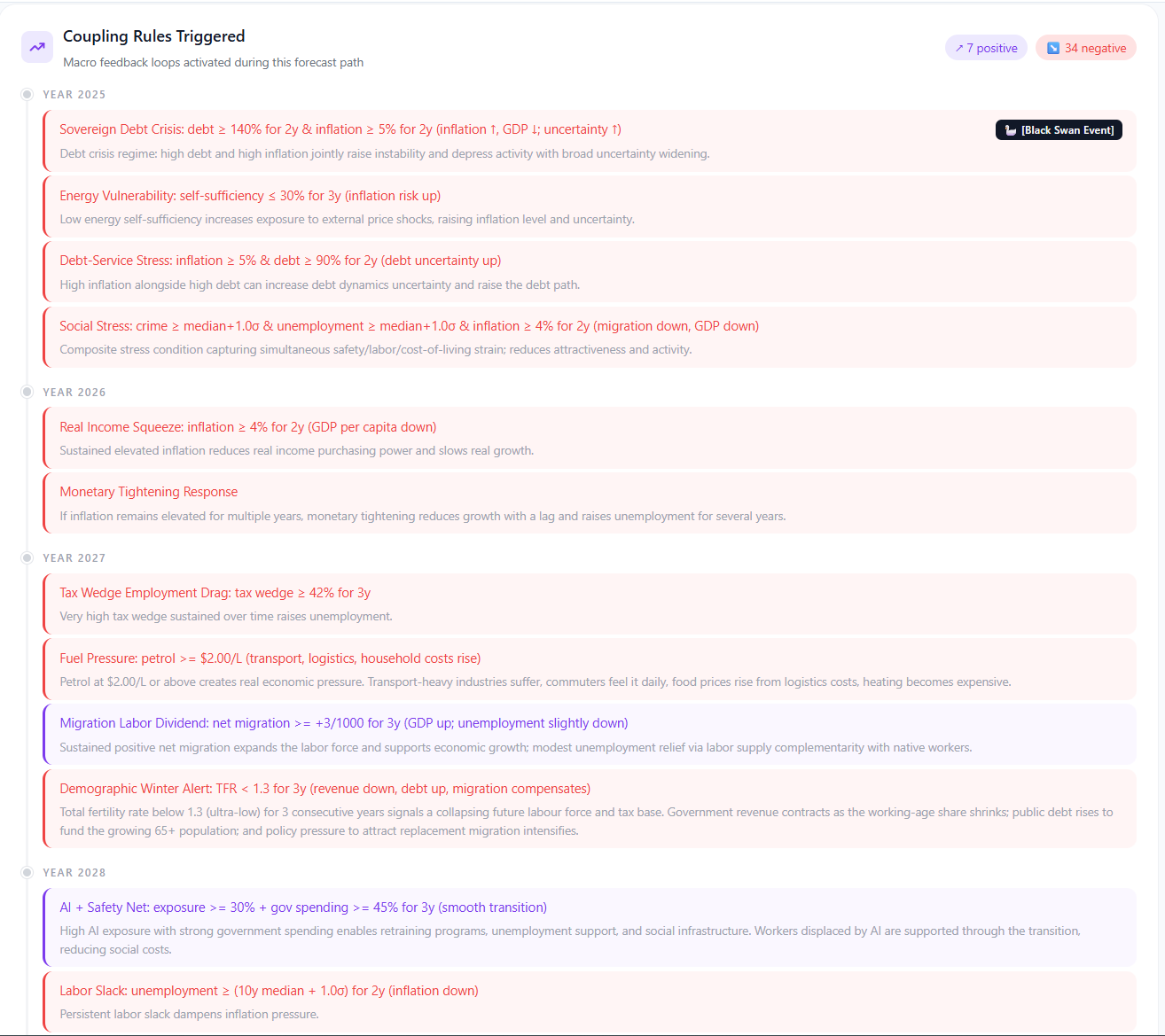

The Structural Cascade: BSE-03 Sovereign Debt Crisis Fires in Year 1

WorldSim's Black Swan Engine triggers BSE-03 (Sovereign Debt Crisis) immediately in 2025. Italy's debt above 140% combined with inflation above 5% crosses the crisis threshold. This activates the most severe coupling cascade: 54 negative rules fire vs only 7 positive. Debt-Service Stress, Social Stress, and Monetary Tightening Response compound the damage. By 2031, Tax Wedge Employment Drag and Demographic Winter Alert join the cascade.

Stressed vs Baseline: Fiscal Score Collapses from 42 to 17

The Comparison Engine puts the stressed Italy (TI 0.43) against the baseline (TI 0.44). Because the tilts revert after 5 years, the 2040 comparison shows partial recovery; the headline gap is just 1 point. But the structural scars are visible in two domains: Fiscal drops from 42 to 37 (the debt overshoot leaves a lasting mark), and Demographics collapses from 25 to 17 (the crisis accelerates brain drain and depresses fertility further). Income, Housing, Labour, Energy, and Technology converge back, confirming that the acute fiscal-demographic damage persists even after the macro shock passes.

Key Takeaway for Macro Investors

This scenario quantifies the Italian sovereign risk that the BTP-Bund spread is trying to price. The P50 median shows debt reaching 167% of GDP, serious but potentially manageable. The P90 tail shows 194%: restructuring territory. The coupling rules reveal that once BSE-03 (Sovereign Debt Crisis) fires, the cascade is self-reinforcing: debt-service costs rise, forcing austerity, which contracts GDP, which worsens the debt ratio further. A macro fund can use WorldSim to quantify not just the direction but the distribution of Italian sovereign risk under any rate + inflation + fiscal configuration, and compare it against any other country in minutes.